You did everything right, you carried insurance, and followed the law. Then someone who doesn’t have vehicle insurance drove into you — and now you’re looking at medical bills, a damaged vehicle, missed work, and the sinking realization that the driver who caused all of it doesn’t have insurance to cover any of it.

This situation is more common in Nevada than most people realize. Despite state law requiring every driver to carry minimum liability coverage, a meaningful percentage of drivers on Las Vegas roads are uninsured. Some let their policies lapse, never carried coverage at all, or some hand over an insurance card at the scene that turns out to be expired or fake.

Discovering the other driver has no valid insurance is not the end of your recovery options. It changes them — significantly — but it doesn’t eliminate them. Understanding exactly what your options are, and moving quickly to protect them, is what separates people who recover fairly from people who absorb losses that weren’t their fault.

Howard Injury Law handles uninsured motorist cases throughout Las Vegas and Nevada. Glen Howard and his legal team are available 24/7. No fees unless we win.

Do This — Even If They Claim to Have Insurance

The steps you take in the minutes after a crash involving an uninsured driver directly affect your ability to recover later. Don’t skip any of them, even if the other driver seems cooperative or insists their insurance is current.

Call 911 and request a police response. A police report is the official record of the crash. It documents the scene, the vehicles, any visible injuries, and the responding officer’s observations. In an uninsured motorist claim, the police report is often the first document your insurance company requests. Without it, establishing what happened and who caused it becomes significantly harder.

Collect the other driver’s information regardless of what they tell you about their insurance. Name, date of birth, driver’s license number, license plate number, vehicle make and model, and any insurance card they provide — even if you suspect it may not be valid. If they claim to be insured, write down the carrier name and policy number they give you. You can verify it later. You can’t verify what you didn’t collect.

Photograph everything. The vehicles, the damage, the license plates, the road conditions, any visible injuries, the intersection or crash location. Take more photos than you think you need. Details that seem obvious at the scene become contested later.

Get witness contact information. Bystanders who saw the crash are valuable in any injury claim. In an uninsured motorist claim, where the other driver may later deny fault or dispute the circumstances, independent witness accounts carry particular weight.

Do not accept cash at the scene in lieu of going through insurance. A driver without insurance may offer to pay you directly to avoid involving law enforcement. That offer almost never materializes in full, it eliminates your ability to document the crash officially, and it leaves you with no recourse if your injuries turn out to be more serious than they appeared.

How to Verify Whether the Other Driver Is Actually Insured

Insurance cards can be expired, forged, or belong to a different vehicle entirely. A driver who hands you a card at the scene may still be uninsured. Here’s how to verify.

Your insurance company can often run a check on the other driver’s coverage once you’ve provided the carrier name and policy number. The Nevada DMV maintains vehicle registration records that include required insurance filings. If the at-fault driver’s vehicle was registered in Nevada, their insurance status may be traceable through official channels.

An attorney can move faster and with more authority on this verification. If the other driver’s coverage turns out to be invalid, your attorney can document that immediately and pivot your claim toward your own UM coverage or other available recovery paths.

Your Own Insurance Is Your Primary Protection: UM/UIM Coverage

The most important protection you can have when hit by an uninsured driver in Nevada is uninsured motorist coverage on your own policy. UM coverage — and its companion underinsured motorist coverage, UIM — is the financial bridge between what the at-fault driver owes you and what they can actually pay.

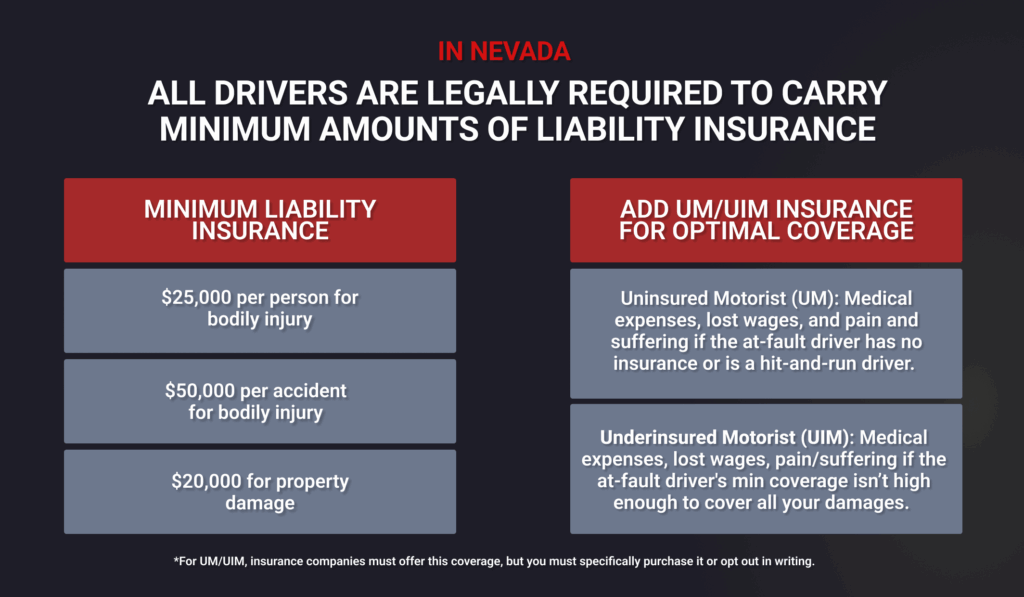

Nevada law requires insurance carriers to offer UM/UIM coverage to every policyholder. You can decline it in writing, but if you didn’t specifically reject it, there’s a good chance you have it. Pull your declarations page and look for it. The coverage limits are listed there.

When the other driver has no insurance, your UM coverage steps in to pay for your medical expenses, lost wages, pain and suffering, and other damages — up to your policy limits. Your own insurer essentially stands in the shoes of the uninsured driver and compensates you as if they were the one paying.

This sounds straightforward. In practice, it’s more complicated. Your own insurance company, despite the fact that you pay them premiums, is still motivated to minimize the amount they pay on a UM claim. They will evaluate your injuries, dispute causation, and argue about the value of your damages just as aggressively as any third-party insurer would. Don’t approach a UM claim assuming your own carrier is on your side.

Understanding exactly how uninsured motorist coverage works in Nevada — what it covers, what it doesn’t, and how to maximize it — is essential reading before you start that claims process.

What If You Don’t Have UM Coverage?

If you declined UM coverage or it’s not part of your policy, your options narrow but don’t disappear entirely.

Your own collision coverage can pay for vehicle repairs regardless of the other driver’s insurance status, subject to your deductible. MedPay — medical payments coverage — can cover initial medical expenses if you carry it. Understanding what MedPay covers and how it works can help you identify resources you may not have realized you had.

Beyond your own policy, you can pursue the uninsured driver directly through a personal injury lawsuit. Nevada courts can enter a judgment against them for the full value of your damages. The practical challenge is collection — a judgment against an uninsured driver is only as valuable as their ability to pay it. Drivers without insurance often don’t have significant attachable assets. Wage garnishment may be available but produces recovery slowly.

That said, lawsuits against uninsured drivers aren’t always futile. Some uninsured drivers have assets, real property, or income that makes collection realistic. An attorney can assess whether pursuing a judgment makes sense in your specific situation.

Nevada’s Penalties for Uninsured Driving — And Why They Matter to Your Claim

Driving without insurance in Nevada carries real consequences. First offense penalties include fines and a license suspension. Repeat offenders face escalating fines, longer suspensions, and potential vehicle impoundment. Nevada maintains a mandatory insurance database that carriers report to, and the DMV can flag uninsured vehicles.

Why does this matter to your claim? Because the documentation of the other driver’s uninsured status — their citation, the DMV records confirming lapsed coverage — becomes part of your case file. It establishes that their failure was not a technical oversight but a violation of Nevada law. In some situations, particularly where the uninsured driver was also at fault in a clear and documented way, that combination strengthens your position in litigation or settlement negotiations.

It also matters for understanding who is liable in a motor vehicle accident in Nevada when the at-fault party lacks coverage. Liability doesn’t disappear because someone is uninsured. The legal responsibility is still theirs. The challenge is the mechanism for collecting on it.

When the Other Driver Has Some Insurance — But Not Enough

A variation of the uninsured problem is the underinsured driver. They carry coverage, but their limits are too low to compensate your actual damages. Nevada’s minimum liability coverage is $25,000 per person for bodily injury. If your medical bills alone exceed that amount — which happens quickly in serious injury cases — the at-fault driver’s policy is exhausted before your losses are covered.

This is where underinsured motorist coverage, the UIM component of your own policy, becomes critical. Once the at-fault driver’s policy pays its limit, your UIM coverage can cover the gap between that amount and your actual damages, up to your UIM policy limits.

The claims process for UIM coverage is similar to UM — your own insurer steps in as the payor and will evaluate the claim with the same scrutiny they’d apply to any other. Having an attorney manage that process protects both the documentation of your damages and the final payout.

If you accepted a settlement from the at-fault driver’s insurer without understanding that UIM coverage was also available, that settlement may have waived your right to pursue the additional coverage. This is one reason why you shouldn’t talk to the insurance company alone after an accident — the decisions made in early conversations can have consequences that aren’t apparent until later.

The Role of an Attorney in an Uninsured Motorist Case

Uninsured motorist claims are not simpler than standard third-party claims. In some ways they’re more complex because you’re negotiating against your own carrier, who has both the financial motivation to minimize payment and the detailed knowledge of your policy’s terms and limitations.

An attorney who handles Nevada motor vehicle accident cases knows how UM claims are evaluated, where carriers apply pressure, and how to present your damages in a way that resists lowball offers. They can also investigate whether other parties might share liability — a vehicle owner who negligently entrusted their car, an employer whose employee was driving uninsured on company time, or other circumstances that create additional recovery paths.

At Howard Injury Law, Glen Howard spent years on the insurance defense side. He has sat in the room where claim values are assigned and knows exactly what that process looks like from the inside. That background changes how he approaches a UM negotiation — and it changes the outcomes for his clients. See what to expect when you call a personal injury lawyer if you’re unsure what that first conversation involves.

Frequently Asked Questions

What if the other driver gives me insurance information that turns out to be fake or expired?

Document what they gave you, report it to the responding officer if police are still at the scene, and contact your own insurance carrier immediately to open a UM claim. Providing false insurance information is a separate violation under Nevada law and can be documented in the police report. An attorney can help you pursue all available recovery paths once the coverage status is confirmed.

Can I sue an uninsured driver directly?

Yes. You can file a personal injury lawsuit against an uninsured at-fault driver and obtain a judgment for your damages. Whether that judgment is collectible depends on the driver’s financial situation. An attorney can assess the practical value of pursuing a direct lawsuit alongside or instead of a UM claim.

Will filing a UM claim raise my insurance rates?

Nevada law provides some protections for policyholders who file UM claims — you were the victim of another driver’s negligence, not the cause of a crash. Whether and how your rates are affected depends on your specific carrier and policy terms. An attorney can advise you on how to manage the claim process in a way that minimizes collateral impact.

What if I didn’t know I had UM coverage?

Check your declarations page — the summary document that lists your coverages and limits. If UM/UIM coverage appears there, you have it. If you’re unsure, call your carrier and ask them to confirm your coverage types and limits before you say anything else about the accident. Then consult an attorney before proceeding with the claim.

How long do I have to file a UM claim in Nevada?

Your UM claim is governed by both your policy’s terms and Nevada’s statute of limitations. Generally, the two-year personal injury deadline applies. Policy terms may impose shorter notice requirements. Contact an attorney promptly — delays can jeopardize coverage that would otherwise be available to you.

Being Hit by an Uninsured Driver Is Unfair — Your Recovery Doesn’t Have to Be

What if the other driver doesn’t have vehicle insurance? It means the standard claims process doesn’t work the way it was supposed to. It means you need to understand your own coverage, move quickly to preserve your options, and avoid the mistakes that cost people real money in exactly this situation.

The motor vehicle accident attorneys at Howard Injury Law handle uninsured and underinsured motorist cases throughout Las Vegas and Nevada. We know how UM claims work, how carriers evaluate them, and how to fight for the full value of what you’ve lost. Start with a free case review — there’s no obligation and no fees unless we recover for you.

You were the one following the rules. You deserve to be made whole.