If you’ve ever looked at your auto insurance policy and thought, “What exactly is UM/UIM—and do I really need it?” you’re not alone. Most drivers in Las Vegas don’t fully understand this coverage until after an accident—when it’s too late to add it.

Injured? Call us at Howard Injury Law 24/7 at (702) 331-5722 for a free consultation or fill out our 24/7 web form.

Here’s the reality: UM/UIM coverage can be the difference between being fully protected… or paying out of pocket after a serious crash.

What Is the Meaning of UM/UIM?

Let’s start simple. UM/UIM stands for:

- UM = Uninsured Motorist

- UIM = Underinsured Motorist

Together, this coverage protects you when the person who caused the accident:

- Has no insurance at all (UM)

- Has insurance, but not enough to cover your damages (UIM)

Think of it as a backup plan when the at-fault driver can’t fully pay. Because yes—this happens more often than people expect in Nevada.

What Does UM Stand for in Insurance?

UM specifically stands for Uninsured Motorist.

This applies when:

- The other driver has no active insurance

- The driver flees the scene (hit-and-run)

- The at-fault party cannot be identified

In these situations, your own policy steps in to cover what the other driver should have paid. Without UM coverage, you could be left handling medical bills, lost income, and recovery costs on your own.

What Does UM/UIM Pay For?

This is where UM/UIM becomes incredibly valuable.

It typically covers:

- Medical expenses

- Lost wages

- Pain and suffering

- Future medical care

- Rehabilitation costs

In other words, it covers the same types of damages you would pursue in a personal injury claim against the at-fault driver.

The difference?

Instead of chasing someone with no money or limited coverage, your own insurance provides the compensation. A skilled Las Vegas personal injury attorney can help structure and negotiate these claims to ensure you receive the full value available under your policy.

Is UM/UIM Worth It?

Let’s be blunt—yes, it’s worth it. Here’s why:

- Around 10.4% of drivers in Nevada are uninsured

- Many insured drivers only carry minimum coverage

- Serious accidents often exceed those limits quickly

That means even if the other driver is “insured,” there’s a strong chance their policy won’t fully cover your damages.

UM/UIM fills that gap. Without it, you’re relying on:

- The other driver’s limited policy

- Or your own finances

From a risk perspective, UM/UIM is one of the smartest coverages you can carry.

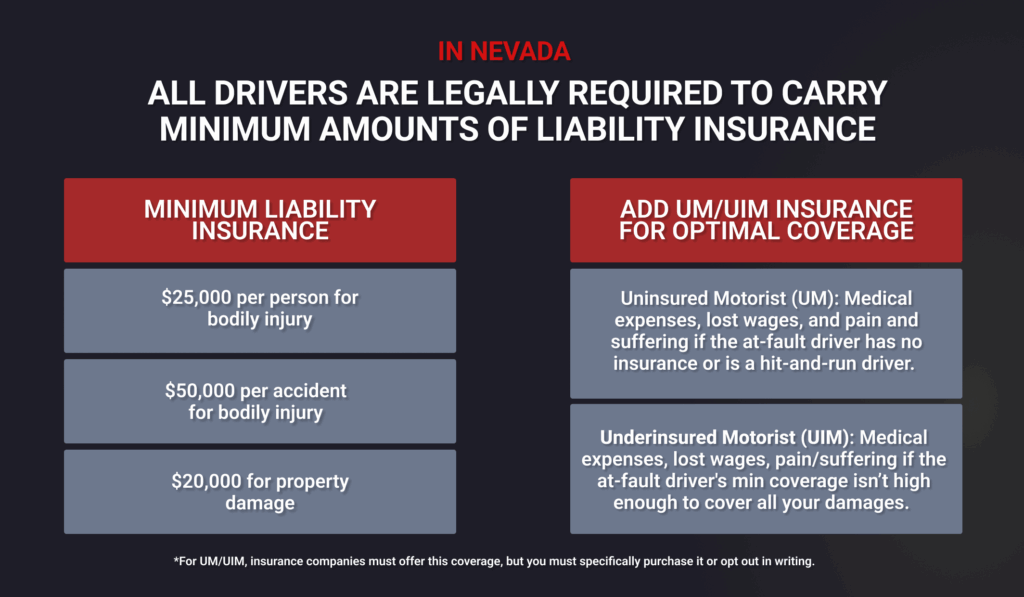

Does Nevada Require Underinsured Motorist Coverage?

No—Nevada does not require UM/UIM coverage.

However, there’s an important detail: Insurance companies are required to offer it when you purchase a policy.

If you choose not to carry UM/UIM, you typically have to:

- Sign a form declining it

- Acknowledge that you understand the risk

Many drivers decline it to save a small amount on premiums… without realizing what they’re giving up. From a legal standpoint, most Nevada accident lawyers strongly recommend carrying it.

Does UIM Stack in Nevada?

Yes—UIM coverage can often stack in Nevada.

“Stacking” means you may be able to combine multiple policies or coverage limits to increase your total available compensation. For example:

- Multiple vehicles on one policy

- Multiple policies within a household

This can significantly increase your recovery in a serious accident. However, stacking rules can be complex and depend on:

- Policy language

- Insurance company terms

- Specific circumstances of the claim

A knowledgeable Las Vegas attorney can review your policy and determine whether stacking applies to your situation.

How Much Is Uninsured Motorist Coverage in Nevada?

The cost of UM/UIM coverage in Nevada is typically surprisingly affordable. On average:

- It may add a modest amount to your monthly premium

- Often far less than the cost of a single emergency room visit

Coverage limits are usually offered in tiers, such as:

- 25/50 (lower limits)

- 50/100

- 100/300 or higher

These numbers represent:

- Maximum payout per person

- Maximum payout per accident

Most insurance professionals—and personal injury lawyers—recommend matching your UM/UIM coverage to your liability limits whenever possible. Because if you’re protecting others at a certain level, you should protect yourself at that same level too.

Which States Require UM/UIM Coverage?

UM/UIM requirements vary across the country. Some states:

- Require uninsured motorist coverage

- Require underinsured motorist coverage

- Or require both

Others—like Nevada—do not require it but mandate that insurers offer it. In Nevada, if you have uninsured motorist coverage, you automatically have underinsurance coverage as well. Underinsurance coverage applies when your damages exceed the at-fault driver’s bodily injury liability limits. It picks up where the other driver’s liability coverage ends.

For instance:

In a scenario where your injury claim is valued at $150,000, with the same coverage limits, you would receive $25,000 from the at-fault driver’s insurance and an additional $25,000 from your underinsurance. The remaining $100,000 would not be covered, as it exceeds both coverage limits.

If your injury claim amounts to $50,000 and the at-fault driver’s policy provides 25/50 bodily injury liability coverage, and you have 25/50 underinsurance coverage, the at-fault driver’s insurance will cover $25,000. Your underinsurance coverage will then cover the remaining $25,000, ensuring full compensation for your claim.

In states where it’s optional, it’s widely recommended due to:

- The number of uninsured drivers

- The financial risk of serious accidents

The takeaway?

Whether required or not, UM/UIM is considered essential protection by most legal and insurance professionals.

Why UM/UIM Matters So Much in Las Vegas

Las Vegas is a unique driving environment.

You have:

- Heavy tourism traffic

- Out-of-state drivers

- Rideshare vehicles

- High-speed roadways

All of this increases the likelihood of accidents involving:

- Uninsured drivers

- Underinsured drivers

- Hit-and-run situations

Combine that with Nevada’s relatively low minimum liability limits, and you get a perfect storm.

A serious accident can easily exceed:

- $25,000 per person

- $50,000 per accident

UM/UIM coverage ensures you’re not left exposed in these situations.

What to Do After an Accident Involving UM/UIM

If you’re involved in a crash where UM/UIM may apply, your actions matter. Here’s what to do:

1. Call 911

Always report the accident.

A police report helps:

- Establish facts

- Document the scene

- Support your claim

2. Seek Medical Attention Immediately

Even if injuries seem minor, get evaluated.

This:

- Protects your health

- Creates medical documentation

- Strengthens your claim

3. Notify Your Insurance Company

You should notify your insurer promptly.

However:

- Avoid giving detailed recorded statements right away

- Avoid speculating about fault

You can initiate the claim without overexplaining.

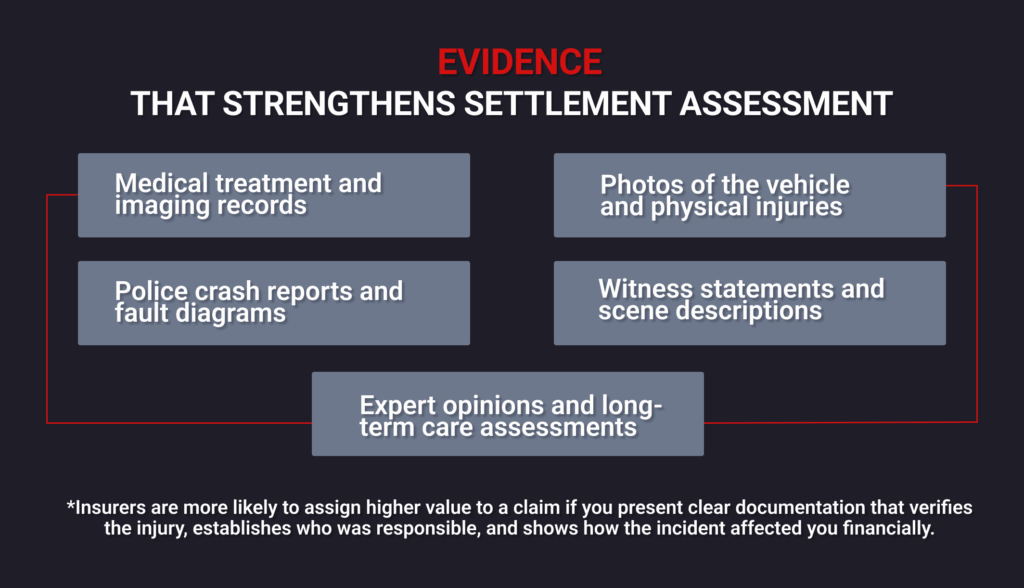

4. Document Everything

Take photos of:

- Vehicle damage

- Injuries

- The accident scene

Keep records of:

- Medical visits

- Expenses

- Missed work

5. Consult a Personal Injury Lawyer

UM/UIM claims are often more complex than standard claims. Insurance companies may:

- Dispute the extent of your injuries

- Challenge liability

- Minimize payout amounts

An experienced Las Vegas car accident attorney can:

- Handle negotiations

- Interpret your policy

- Maximize your recovery

The Reality of UM/UIM Claims

Here’s something most people don’t expect.. Even though you’re dealing with your own insurance company, UM/UIM claims can still become adversarial.

Why? Because the insurance company is now paying out of its own pocket. That means:

- They may scrutinize your claim more closely

- They may challenge damages

- They may try to settle for less

This is where having legal representation becomes critical. A strong attorney understands how to:

- Present your claim effectively

- Push back against low offers

- Ensure you receive fair compensation

Common Misconceptions About UM/UIM

Let’s clear up a few myths.

“I don’t need it because I’m a safe driver.”

UM/UIM protects you from other drivers—not yourself.

“Health insurance will cover everything.”

Health insurance does not cover lost wages or pain and suffering.

“The other driver’s insurance will handle it.”

Not if they don’t have enough coverage.

“It’s too expensive.”

Compared to the financial risk, UM/UIM is relatively low cost.

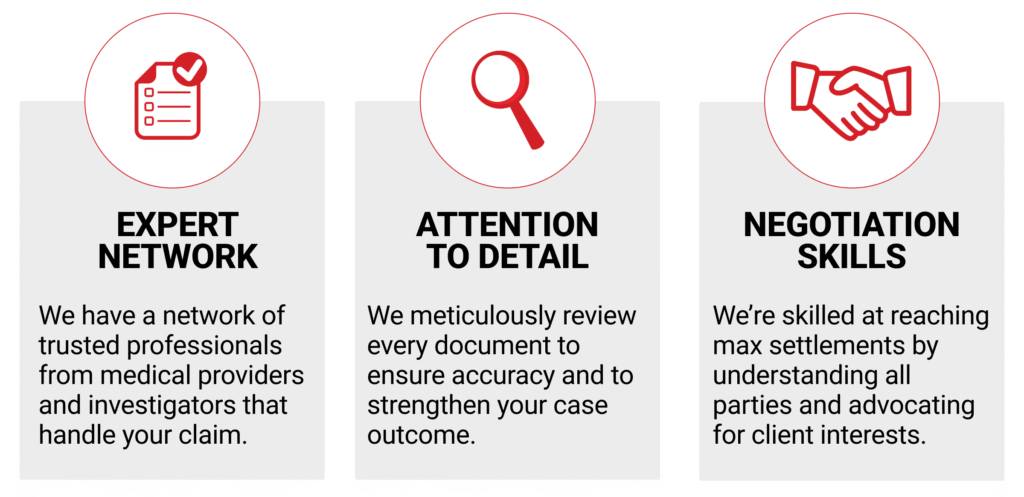

How a Las Vegas Lawyer Can Help With UM/UIM Claims

Handling a UM/UIM claim without guidance can be overwhelming.

A skilled Las Vegas personal injury lawyer can:

- Review your insurance policy in detail

- Identify all available coverage

- Determine whether stacking applies

- Handle all communication with insurers

- Build a strong damages case

- Negotiate aggressively on your behalf

At Howard Injury Law, the focus is on protecting clients from the tactics insurance companies use to reduce payouts. Because at the end of the day, your recovery should not be limited by someone else’s lack of insurance. UM/UIM coverage is one of those things people don’t think about—until they wish they had it.

It’s not about expecting the worst. It’s about being prepared for it.

In a city like Las Vegas, where accidents happen every day and not everyone carries adequate insurance, UM/UIM is more than optional coverage. It’s protection.

Injured in Las Vegas? Speak Directly with an Attorney. At Howard Injury Law, we represent all injury victims across Las Vegas, Nevada with elite trial experience and real courtroom strength. When your health, income, and future are at stake, you deserve a lawyer who prepares every case as if it’s going to trial.

📞 Free Consultation: (702) 331-5722

–Se habla español

-我们说普通话和粤语

Learn More About:

-Our Las Vegas car accident attorneys

-How to choose the right personal injury lawyer in Las Vegas

–Helpful resources before and after an accident

Learn about Attorney Glen Howardand the team behind Howard Injury Law.

Find us on Google, Yelp, or follow us on Instagram for community news, legal updates, and safety tips.