When it comes to personal injury claims in Las Vegas, intimate knowledge of Nevada insurance law isn’t just a credential — it’s the difference between an attorney who understands the system and one who’s learned to fight against it without ever seeing how it works from the inside.

Most personal injury attorneys in Las Vegas understand Nevada insurance law the same way a plaintiff understands a game — by playing against the other side and learning the rules from experience.

Howard Injury Law’s attorneys learned it differently. They learned it from the inside — working on the defense side of personal injury claims, evaluating files from the insurer’s perspective, building the arguments that minimize payouts, and understanding exactly how insurance companies make decisions about what cases are worth.

That inside knowledge is what intimate knowledge of Nevada insurance law actually means in practice. Not just knowing the statutes — knowing how insurance companies use them, bend them, and in some cases violate them. Here’s why that distinction matters for your personal injury case in Las Vegas.

How Nevada Insurance Law Shapes Every Personal Injury Claim

Nevada’s insurance regulatory framework under NRS Title 57 governs how insurance companies must handle claims — from the initial investigation through final settlement. These aren’t abstract rules. They create specific obligations on insurers and specific rights for injured claimants that directly affect the trajectory and value of every personal injury case.

The 80-Day Settlement Window

Nevada law imposes a mandatory timeline on auto insurance claim settlements. Once liability is reasonably clear and damages are documented, insurers have a defined window to settle claims fairly. Violations of this timeline don’t just affect the individual claim — they expose the insurer to bad faith liability.

Most claimants don’t know this timeline exists. Most insurers count on that. An attorney with intimate knowledge of Nevada insurance law monitors these timelines from day one — not reactively when the insurer stalls, but proactively as a tool for managing the claim’s trajectory and building leverage.

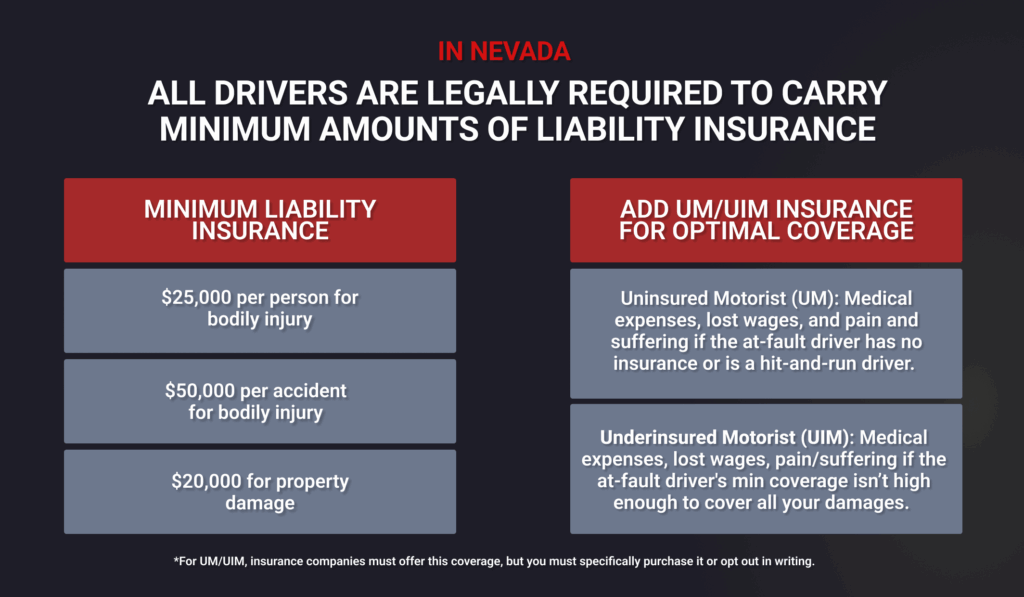

Nevada’s Minimum Coverage Requirements

Nevada requires drivers to carry minimum liability coverage — currently $25,000 per person and $50,000 per accident for bodily injury, plus $20,000 for property damage. These are the floors, not the ceilings. Many drivers carry only minimum coverage.

Understanding coverage limits before building a demand is essential. An attorney who doesn’t know the applicable limits going into negotiation can’t assess whether the insurer’s offer reflects genuine coverage constraints or a deliberate undervaluation. The distinction determines your strategy — whether to pursue a policy limits demand, explore umbrella coverage, or look at additional liable parties.

Uninsured and Underinsured Motorist Coverage

Nevada law requires insurers to offer UM/UIM coverage to every policyholder. If the at-fault driver has no insurance or insufficient insurance to cover your damages, your own UM/UIM coverage becomes your primary recovery source.

Navigating UM/UIM claims involves making a claim against your own insurer — which creates a conflict of interest that many claimants don’t anticipate. Your insurer is obligated to pay your valid claim but has a financial incentive to minimize it. An attorney who understands how UM/UIM claims are evaluated internally — and what arguments insurers use to reduce them — enters that negotiation with a significant advantage over one who doesn’t.

What Insurance Bad Faith Means for Your Case

Nevada’s Unfair Claims Settlement Practices Act under NRS 686A.310 imposes specific obligations on insurers in how they handle claims. Violations of those obligations can constitute insurance bad faith — and bad faith carries consequences that extend beyond the original claim value.

What Constitutes Bad Faith in Nevada

Insurance bad faith occurs when an insurer unreasonably denies, delays, or undervalues a valid claim without a legitimate basis. The key word is unreasonably — an insurer has the right to investigate and contest claims. What they don’t have the right to do is misrepresent policy provisions, fail to conduct prompt investigations, or make lowball offers that don’t reflect a genuine evaluation of claim value.

Specific practices that can constitute bad faith in Nevada include misrepresenting the facts of a claim or applicable policy provisions, failing to acknowledge and act promptly on communications about a claim, not attempting to settle claims promptly when liability is reasonably clear, and compelling claimants to initiate litigation to recover amounts clearly owed under the policy.

Why Insurance Defense Experience Matters Here

Identifying bad faith conduct requires knowing what proper claims handling looks like from the inside. An attorney who has worked in insurance defense knows the internal processes, the documentation requirements, and the standards adjusters are supposed to meet. When an insurer deviates from those standards — whether through stalling, misrepresentation, or lowball offers — an attorney with that inside perspective recognizes it immediately.

That recognition changes the dynamic. It converts a routine negotiation into a conversation where the insurer knows their conduct is being evaluated against the standards they’re required to meet — not just argued about abstractly.

Damages Available in Bad Faith Cases

When an insurer acts in bad faith in Nevada, the remedies available to the claimant can extend beyond the original policy limits. Consequential damages — losses caused by the insurer’s bad faith conduct — and in cases of particularly egregious conduct, punitive damages may be available.

This is not a routine path in most personal injury cases. But an attorney who recognizes bad faith conduct when it occurs — rather than accepting unreasonable denials or delays as normal — protects your ability to pursue those remedies if the circumstances warrant.

How Insurers Actually Evaluate Claims — The Inside View

Understanding Nevada insurance law statutes is one thing. Understanding how insurance companies actually apply those laws in their internal claim evaluation is something different — and it’s where intimate knowledge of the defense side produces the most direct case value.

How Adjusters Build Their Files

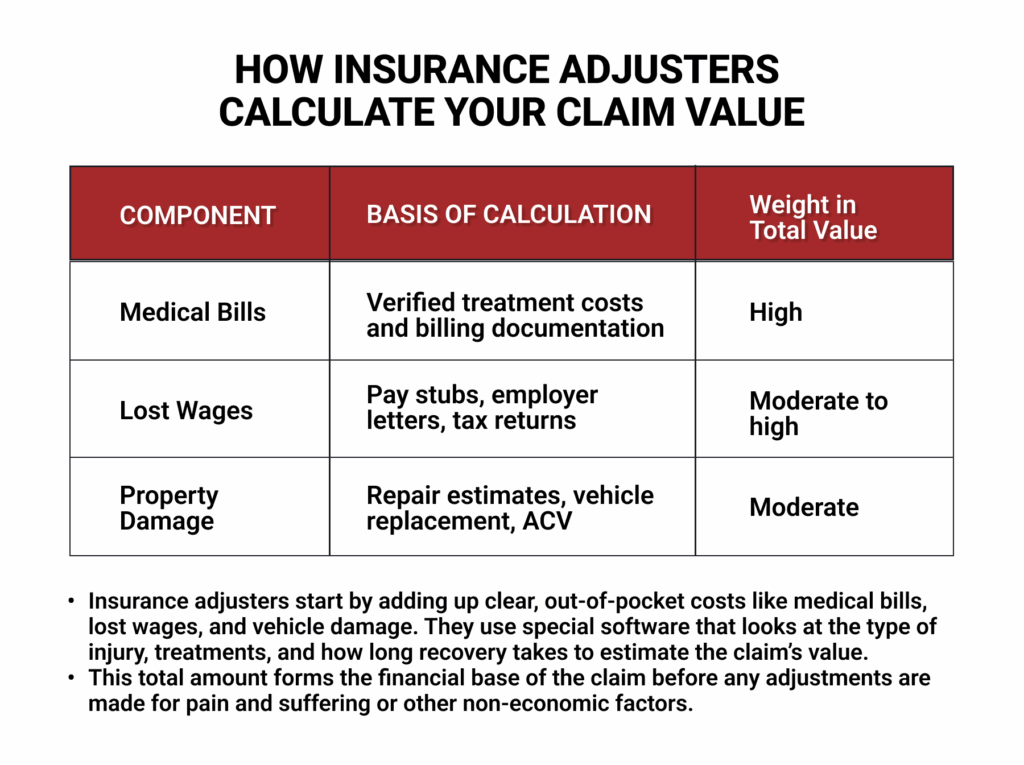

Insurance adjusters work from a file — a collection of documents that shapes their evaluation of what a claim is worth. The police report, the medical records, the recorded statement if there is one, surveillance if they’ve conducted it, and any social media activity they’ve found. Every document in that file either supports or undermines the claim value.

An attorney who has built defense files knows exactly what adjusters look for to minimize claims. They know how soft tissue injuries get categorized internally and what pushes a claim from low to high severity in the adjuster’s evaluation system. They know when an offer reflects genuine case assessment and when it’s a negotiating tactic.

That knowledge shapes how plaintiff cases get built. Not reactively — filling gaps after the insurer has already made their arguments — but proactively, building documentation that addresses adjuster evaluation criteria from the beginning.

How Insurers Respond to Trial-Ready Attorneys

Insurance companies maintain internal data on law firms and individual attorneys. Their evaluation of any claim is influenced by who is on the other side — specifically, whether that attorney is genuinely prepared to file a lawsuit and try the case to verdict if settlement negotiations fail.

An attorney whose intimate knowledge of Nevada insurance law includes how insurers assess litigation risk is better positioned to apply that leverage strategically. Knowing when an insurer is bluffing with a low offer — versus when their position reflects a genuine coverage or liability dispute — is information that changes negotiation strategy.

For more on how this dynamic affects settlement outcomes and why trial readiness amplifies it, read our guide on elite trial strength and what it means for your Las Vegas personal injury case.

Nevada Insurance Law and Specific Case Types

Intimate knowledge of Nevada insurance law manifests differently across different personal injury case types — because the insurance landscape varies significantly by accident type.

Auto Accident Cases

Auto liability claims in Nevada involve the at-fault driver’s liability coverage, your own UM/UIM coverage if applicable, and potentially MedPay if your policy includes it. Each of these coverage types has its own claim process, timeline obligations, and documentation requirements under Nevada law.

An attorney who understands how each coverage type works — not just theoretically but from the perspective of how insurers process those claims internally — manages multi-coverage situations more effectively than one approaching it purely from the plaintiff side.

Rideshare and Commercial Vehicle Cases

Rideshare accidents involve layered insurance — the driver’s personal policy, the rideshare company’s commercial policy, and coverage that varies depending on whether the driver was actively on a trip. Commercial truck accidents involve federal motor carrier regulations alongside Nevada insurance requirements, with coverage obligations that can be significantly higher than standard auto minimums.

Knowing how these layered coverage situations work from the inside — which policy activates when, how carriers in a multi-policy situation interact, and what arguments each insurer is likely to make about the other’s primary coverage obligation — is a specific advantage in these more complex cases.

Premises Liability Cases

Casino and resort accidents in Las Vegas involve commercial general liability policies with coverage limits, claims processes, and internal evaluation criteria that are materially different from auto liability. Nevada’s gaming properties are among the most sophisticated insurance risk managers in the country. Knowing how their claims departments operate is part of what effective representation in Las Vegas premises liability cases requires.

What to Ask Any Attorney About Their Insurance Knowledge

When you’re evaluating personal injury attorneys in Las Vegas, the question of insurance law knowledge is worth exploring specifically — not just accepting general assurances about experience.

Ask directly: have you worked on the insurance defense side of personal injury claims? The answer is either yes or no — and the difference is significant.

Ask: how does your knowledge of how insurers evaluate claims affect how you build cases from day one? An attorney who understands this answers with specifics about documentation strategy, demand timing, and negotiation positioning. An attorney who doesn’t understand it gives a general answer about fighting for clients.

Ask: what happens when you believe an insurer is acting in bad faith on my claim? The answer should demonstrate familiarity with Nevada’s bad faith framework and when it becomes relevant — not just a vague reference to taking action if the insurer misbehaves.

For a complete framework for evaluating any attorney’s knowledge and approach before you hire, read our guides on questions to ask during a personal injury consultation and red flags when hiring a personal injury lawyer.

How Howard Injury Law’s Insurance Defense Background Applies

Glen Howard’s direct experience on the insurance defense side means your case gets built differently from day one.

Documentation is assembled with adjuster evaluation criteria in mind from your very first appointment — not pieced together after the insurer has already made their arguments. Demand packages are structured to address the defense’s anticipated positions before they’re raised, not in reaction to them. And when the insurer makes an offer, Glen knows whether it reflects a genuine coverage constraint or a test of whether your attorney will actually litigate.

That’s not a subtle difference. It’s the difference between an attorney who responds to the insurance company’s strategy and one who anticipates it.

And it means that when an insurer’s conduct crosses into bad faith territory — unreasonable delays, misrepresented policy provisions, offers that bear no relationship to documented claim value — that conduct is recognized and addressed rather than absorbed as a normal part of the process.

For more on how this differentiator shows up across the full comparison between Howard Injury Law and other Las Vegas personal injury firms, read our guide on why Las Vegas injury victims choose Howard Injury Law.

Frequently Asked Questions

What is Nevada’s bad faith insurance law?

Nevada’s Unfair Claims Settlement Practices Act under NRS 686A.310 requires insurers to handle claims in good faith — conducting prompt investigations, making fair settlement offers when liability is clear, and not misrepresenting policy provisions. Violations can expose the insurer to damages beyond the original policy limits.

What are Nevada’s minimum auto insurance requirements?

Nevada requires minimum liability coverage of $25,000 per person and $50,000 per accident for bodily injury, plus $20,000 for property damage. These minimums apply to all registered vehicles in Nevada. Many drivers carry only the minimum — which is why UM/UIM coverage on your own policy is an important protection.

Can I file a complaint against an insurance company in Nevada?

Yes. The Nevada Division of Insurance handles consumer complaints against insurers at doi.nv.gov. Filing a complaint doesn’t replace legal representation — but it creates a formal record of the insurer’s conduct that can be relevant in bad faith proceedings.

How does insurance defense experience help a plaintiff attorney?

It provides a specific understanding of how claims are evaluated, documented, and decided internally — knowledge that shapes how plaintiff cases are built, how demands are structured, and how negotiation is conducted. The majority of personal injury attorneys learn about insurers from the outside. Defense experience means learning from the inside.

Does Nevada require uninsured motorist coverage?

Nevada requires insurers to offer UM/UIM coverage to every policyholder. Policyholders can waive it in writing — but if you didn’t explicitly waive it, you likely have it. Check your declarations page or call your insurer to confirm your coverage before you need it.

The Inside Advantage

Intimate knowledge of Nevada insurance law is what separates an attorney who fights against the insurance system from one who understands how it actually works — and uses that understanding to build cases that produce better outcomes.

Every document in your file, every demand letter sent, every negotiation position taken is shaped by how well your attorney understands the system on the other side of the table.

Howard Injury Law brings that inside knowledge to every case in Las Vegas. Free consultations 24/7. Call (702) 331-5722 or contact us here.